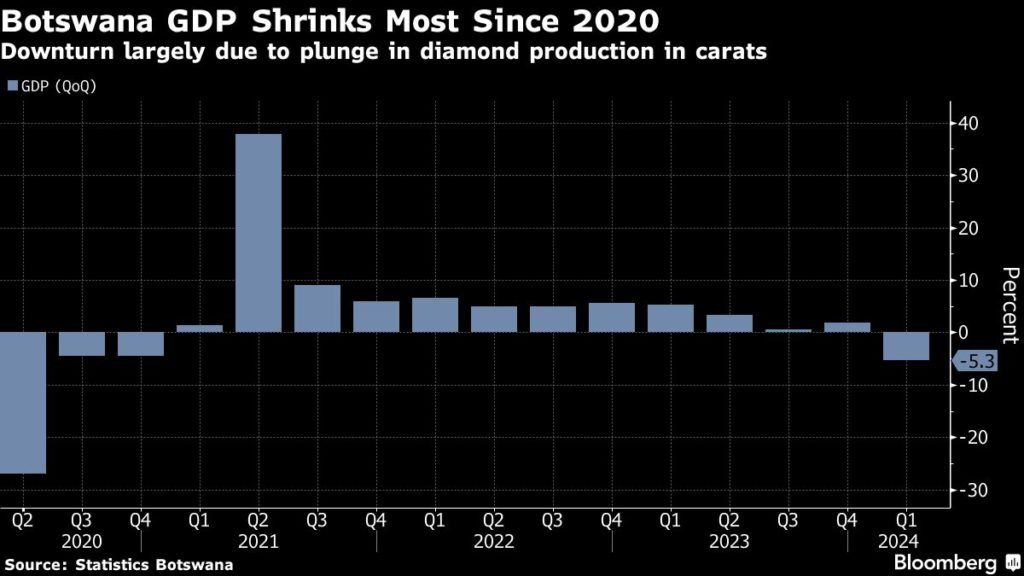

Botswana’s economy contracted by the most since the peak of the pandemic in early 2020, after diamond production plunged.

Gross domestic product shrank an annual 5.3% in the first quarter, compared with growth of 1.9% in the prior three months.

The downturn was primarily influenced by a decrease in real value added of the diamond traders and mining & quarrying industries of 46.8% and 24.8% respectively, Statistics Botswana said in a report Friday.

Botswana is the world’s largest producer of rough diamonds by value, with the revenues making up the bulk of the southern African country’s budget receipts. The decline is likely to make meeting its fiscal targets for this year difficult. The central bank already warned last week that the government would probably miss its economic growth forecast of 4.2% because of weaker mining output.

The global diamond industry almost came to a standstill in the second half of last year as De Beers and Russia’s Alrosa PJSC — the two biggest miners — all but stopped supplies in a desperate attempt to stem a slump in prices. That hit earnings at De Beers, which mines more than three-quarters of its diamonds in Botswana.

Earlier this year De Beers said it expects any recovery in the beleaguered diamond market to be slow and gradual as the industry continues to suffer from weak economic growth in key markets such as China and the US.

Petra Diamonds revised on Thursday its guidance for the next two fiscal years and appointed a new finance leader as part of its plans to lower expenses and debt in a clear sign the diamond market remains in bad shape.

The South African miner had anticipated in December that the sector was beginning to recover. Six months later, Petra has instead cut its production targets. It now expects to produce between 2.8 million and 3.1 million carats in fiscal 2025 and between 2.9 million and 3.3 million in fiscal 2026. This represents a reduction of 18% and 19%, respectively, on the prior target-ranges’ midpoint.

The company also said it expected total carat recovery to be at the lower end of its target range of 2.74 million to 2.78 million for the current fiscal year.

These downgrades, announced in an investor day presentation, coincide with Petra’s plan to reduce operating costs by $30 million annually starting in the fiscal year that ends on June 30, 2025. Total capital spending will be reduced this year to $100 million from the total spent in 2023, which was $117.1 million.

“We have worked hard to deliver an updated business profile in response to ongoing market challenges and to further enhance our resilience to future market and capital cycles,” chief executive Richard Duffy said in a statement.

Petra’s revisions come just a day after the world’s largest diamond producer by value, De Beers, posted disappointing results for its latest sales for the second time this year, and as Anglo American (LON: AAL) plans to sell it off.

New CFO

Petra announced it had appointed Johan Snyman to take on the role of chief financial officer starting from October 1. Snyman will replace Jacques Breytenbach, who will leave his position as CFO and director at the end of September due to personal reasons.

“[Snyman] has played a crucial part in the progress of Petra since joining in January, and I am excited to collaborate with him in his new capacity,” Duffy said.

The new CFO joined Petra this year as financial controller, having worked as vice president for financial reporting at AngloGold Ashanti (NYSE: AU). He has also previously held various financial roles in the mining sector.

Expansions unaffected

Despite the challenging market, Petra remains committed to expanding its Finsch and Cullinan mines in South Africa, it said, and it is projecting production to reach between 3.4 to 3.7 million carats by 2028.

Cullinan is Petra’s flagship mine and the source iconic diamonds, including the famed 3,106-carat Cullinan diamond, which was cut to form the 530-carat Great Star of Africa. They are the two largest diamonds in the British Crown Jewels.

The Cullinan mine is also a source of rare blue diamonds.

Petra’s planned output increase, equivalent to 15% to 17% over three years, will require about $100 million annually. Duffy stated the plans will be financed internally.

Cullinan mine-life can be potentially extended beyond 2048. Finsch, South Africa’s second largest diamond operation by output, could be producing until around 2038.

Shares in Petra experienced high volatility in London after the announcements and were last down 1.96% to 40 pence. This leaves the miner with a total market capitalization of £78.63 million (about $100m).

Naturally fluorescing rough diamond parcel from the Gahcho Kué mine. Credit: Mountain Province Diamonds

De Beers Group and Mountain Province Diamonds announced that their joint venture Gahcho Kué diamond mine has surpassed the C$2 billion spending threshold with Northwest Territories and Indigenous business.

The milestone represents 61% of the total C$3.2 billion spent on the project since 2015 when construction began. Local businesses supply welding, transportation logistics, trucking, passenger and cargo flights, labour, and camp catering. The venture has a stated goal of sourcing at least 60% of its requirements for the project from local businesses.

According to the NWT Bureau of Statistics, diamond mining is the largest contributor to the territory’s gross domestic product – C$588 million out of C$4.25 billion in 2023.

Key elements of the economic contribution of the Gahcho Kué mine include:

Gahcho Kué has a tiered contracting structure that gives preference to Indigenous and NWT businesses. Since 2006, C$5.3 billion has been spent with local and Indigenous business in the Northwest Territories and northern Ontario by Gahcho Kué and De Beers Group’s wholly owned Snap Lake (NWT) and Victor (Ontario) mines. (Snap Lake and Victor are now in active closure). In 2023, 69% of the Gahcho Kué mine spend was with NWT and Indigenous companies, totalling C$228 million, the highest amount spent with NWT businesses since construction. In 2023, C$90 million was spent with companies operated by the mine’s impact benefit agreement (IBA) communities. From 2006 to 2023, Gahcho Kué and Snap Lake mines have contributed a combined C$26.5 million in social investment within the NWT. Gahcho Kué has also made significant payments to Indigenous communities in terms of six IBAs and has paid resource royalties to the government of the NWT. Gahcho Kué was officially opened in 2016 and now provides 663 full-time equivalent jobs, including 245 jobs held by NWT residents.

The mine is located about 280 km northeast of Yellowknife, NWT, on the traditional territories of Tlicho, Dene and Metis peoples. De Beers is the 51% owner and operator. Mountain Province retains the remaining 49%.

In 2023 the project mined 3.3 million tonnes of kimberlite and recovered nearly 5.6 million carats (on a 100% basis). Guidance for 2024 is 4.2 million to 4.7 million carats.

Lucapa today (25 June) announced the sale of its 70 per cent stake in the Mothae mine, in Lesotho, to a local contractor for a nominal sum.

The Australian miner said it wanted to to focus on its core assets in Africa, where it has a 40 per cent stake in the Lulo alluvial mine, in Angola, and in Australia.

Mothae has produced over 150,000 carats since it started commercial production in 2019, bringing in more than $100m in revenue.

Lucapa says it will sell its stake in stake in Mothae Diamonds (Pty) Ltd to Lephema Executive Transport (Pty) Ltd, which has provided it with long-term contract mining services, for A$10,000 (US$6,660).

Mothae Diamonds, which owns the site, will pay Lucapa A$1m (US$666,000) in outstanding technical services payments.

“This agreement is the result of a period of offer and negotiation involving Lucapa and several interested parties,” said Lucapa managing director and CEO Nick Selby.

“(Lephema) Executive has a successful history with the Mothae Diamond Mine, having provided long-term contract mining services. Lucapa wanted to, as far as possible, see

this mine continue to operate and Executive are best placed to achieve this.

“The signing of this agreement is a key step towards Lucapa streamlining its portfolio and executing the new strategy which will focus on assets in Australia and Angola”.

Mothae has indicated resources of 180,000 carats and inferred resources of 960,000 carats, according to December 2023 figures provided by Lucapa, with a modelled per carat value of $606.

Lucapa said in its sales material that Mothae has recovered 13 +100ct diamonds (largest Type IIa gem 213cts), and 10 diamonds valued at over $1m.

Russia is seeking to strengthen ties with Brazil, India, China, and South Africa and other BRICS countries in response to tighter sanctions on diamonds from the G7 and EU.

Setting an agenda for “equal and fair interaction between the parties involved in all segments of the global diamond trade” was the focus of a roundtable discussion at the St. Petersburg International Economic Forum earlier this month.

Russia currently chairs BRICS (the initial letters of Brazil, Russia, India, China, and South Africa. Later additions are Iran, Egypt, Ethiopia, and the United Arab Emirates).

“The only universal mechanism for regulating the global diamond trade, the Kimberley Process Certification Scheme (KPCS), is being undermined by the attempts of numerous countries to introduce unilateral trade barriers,” said BRICS in a statement. Alrosa CEO Pavel Marinychev said: “New cooperation mechanisms will ensure the stability of the global diamond market and preserve the system of the free global trade of diamond products based on the core principles of the Kimberley Process.”

Russia warned back in November 2023 that sanctions on it diamonds would have a “boomerang” effect – harming the countries that imposed them more than Russia itself.

Nikolayev Aysen, head of Russia’s Yakutia republic, where state-controlled diamond miner Alrosa is based, told the BRICS audience: “Given the illegal unilateral restrictions that certain Western countries have imposed on Russian diamonds, it is crucial for us to support the efforts of ALROSA, which aim to diversify international supply markets. For example, this will make it possible to maintain the sustainable socioeconomic development of Yakutia.”

US Capitol building at sunset, Washington DC, USA.

US jewelers have warned Congress of the harm that new sanctions on Russian diamonds will cause for the entire retail sector.

The trade association Jewelers of America (JA) met with with a dozen Democratic and Republican lawmakers in both the House and Senate to voice concerns over the 1 September restrictions that will require all goods of 0.50-scts and above to enter G7 countries via Antwerp for verification.

They say a single import channel will “cause maximum damage to the global diamond and jewelry supply chain, while having minimal effect on Russia’s diamond revenues”.

JA is urging all its members to lobby Congress and explain that the way the restrictions are being implemented will hurt jewelry businesses.

“JA has been working tirelessly behind the scenes and this visit to Washington, D.C. was a critical step to ensure we minimize unnecessary disruptions to the U.S. diamond industry,” said JA president & CEO David J. Bonaparte.

He and fellow JA representatives also called for a “grandfathering” clause to cover goods imported before 1 March (when the 1.0-cts and above restriction was imposed) and for clearer guidance on whether the current size limit applied only to individual, loose diamonds or to the total weight of all diamonds in finished jewelry.

Bruce Cleaver, former CEO at De Beers Group, has been appointed chair and independent non-executive director of Gemfields, the UK-based emerald and ruby miner.

He said the company, founded in 2005, was bringing sophistication to a fragmented and informal colored gemstone industry, much as De Beers did more than a century ago for diamonds.

Cleaver, 59, (pictured) served as De Beers CEO from 2016 until his resignation in February 2023, during which time the company launched its Lightbox range of lab growns and extended its diamond mining agreement with the Botswana government for a further 10 years.

“The parallels with De Beers’ origins and how consistent and reliable supply can deliver remarkable industry growth and positive contributions to communities, are clear to all,” he said.

“The coloured gemstone market has long transcended the arrival of their lab-grown counterparts, with lab-grown rubies having been around for more than 120 years.”

Gemfields operates the Kagem emerald mine and Montepuez, the world’s largest ruby mine, in Mozambique. It holds a 75 per cent stake in both.

Construction of a new processing plant at Montepuez, which will triple its throughput capacity, is due to complete in the first half of 2025.”

Gemfields reported near-record revenues of $262m for FY2023.

Cleaver will replace Martin Tolcher as chair, and Lumkile Mondi who was lead independent non-executive director, effective 1 July.

De Beers, which created the global market for diamond engagement rings through its “A Diamond is Forever” campaign, is shifting back to its marketing roots as its parent company Anglo American (LSE: AAL) moves to sell it off.

Its new ‘Origins’ strategy is part of a wider pivot back towards natural diamonds, announced on May 31. The move makes sense because marketing has always set the diamond sector apart from other mineral industries and the industry risks losing its way if it becomes focused only on mining and turns away from the demand creation side, New York City-based diamond analyst Paul Zimnisky told The Northern Miner.

SIGN UP FOR THE PRECIOUS METALS DIGEST

“Marketing is what moves the needle,” he said. “You can throw money at the problem, you can create demand if the products are marketed properly. You have to look at it as a luxury product, not as a commodity.”

In announcing the divestiture of De Beers on May 14, Anglo said the move would give both companies “a new level of strategic flexibility to maximize value” for Anglo American and the government of Botswana, which each hold 85% and 15% stakes, respectively, in the diamond company. The Botswana government also indicated on June 10 that it wants to increase its interest in De Beers. High capital needs and declining diamond supply present further challenges in the diamond sector, analysts say.

Anglo’s announcement of its De Beers plans, as well as plans to sell off its South Africa-based Anglo American Platinum (JSE: AMS) and its steelmaking coal assets was triggered by BHP’s (ASX: BHP) unsuccessful, multi-billion-dollar acquisition bid in mid-May.

‘Growing desire’ De Beers is also suspending its Element Six lab-grown diamonds (LGD) subsidiary for jewelry to focus instead on synthetic diamond technology for industrial applications, it said in May. Production for the Lightbox LGD brand will stop in a few months, De Beers CEO Al Cook said in a June 13 interview with diamond news site Rapaport.

“The outlook for natural diamonds is compelling,” Cook said in a news release, adding that the company’s new approach will involve “growing desire for natural diamonds through the reinvigoration of category marketing, embracing new approaches that maximize reach and impact.”

Cook explained to Rapaport the need to tell better diamond stories is greater now that “there are more diamonds above the surface of the Earth than below the surface. Every year, diamond mines are closing.”

De Beers first entered the synthetic diamond jewelry market in 2018. In setting up a solid difference between mined and lab-grown diamonds, the company initially offered Lightbox jewelry for up to 80% less than its competitors’ prices.

Slowing sales, production The stronger emphasis on marketing also comes as De Beers grapples with lower sales, with Cycle 4 rough diamond sales, at $380 million this year, down by 20% from last year’s Cycle 4 period of $479 million, the company reported on May 23. The Cycle 4 period approximately covers two weeks in May. Cook said the sales were due to the seasonally slower second quarter and less trading in India during the elections.

Production declined 8% to 31.9 million carats in 2023, from 34.6 million carats in 2022. First quarter output this year, at 6.8 million carats, was down 23% from the year-earlier figure of 8.9 million carats.

The wider industry is also facing the challenge of lower demand, especially in the United States and China. Amid the slow demand, De Beers cut the price of 0.75-carat stones by 4% to 6% at this year’s fourth trading session, according to a May 7 report from Rapaport. In the first sale of the year, the company cut prices by about 10%.

The issue of declining production could be expensive for De Beers to deal with, BMO Capital Markets diamonds analyst Raj Ray implied.

“From mining business point of view, not having a parent company like Anglo American backing De Beers could have some serious implications for diamond supply going forward,” he said.

Rough diamond supply has dropped to around 120 million carats from 150 million carats in 2017-2018, Ray said. It’s expected to drop even more in the next four to five years.

Amid the supply constraints, De Beers has invested $1 billion in expanding the life of its flagship Jwaneng mine in Botswana, and $2.3 billion to move underground the Venetia mine in South Africa.

“The next 12 to 24 months don’t look great for the rough diamond industry,” Ray said. “Anyone looking at De Beers will have to acknowledge (that). There’s huge capital investments that are needed over the next few years across mines to be able to maintain supply, forget about growing supply.”

But despite that hurdle, Ray and Zimnisky both see De Beers maintaining its 30% share of the global diamond market.

“They’ll continue to be the pre-eminent producer in the world,” Ray said. “Anyone who will buy (De Beers) will continue to fund its projects. I don’t see any significant drop in production from the De Beers portfolio.”

Going solo? Once De Beers formally leaves Anglo as part of the company’s restructuring, which CEO Duncan Wanblad has said could take 18 to 24 months to complete, the diamond miner will face the prospect of being purchased or going alone.

Zimnisky said either option has its own difficulties.

“This is something Anglo has wanted for a while,” he said. “They wanted Anglo to become more of a pure play copper producer, or a green infrastructure buildout commodity producer hoping it would lead to a higher valuation for the company. That said, De Beers is a complicated business and not easy to sell. It has (the) Debswana joint venture, which is the crown jewel of the company.”

Ray agrees that few potential buyers would have interest in a company like De Beers whose business requires massive capital investments. An IPO is also unlikely, he said.

“There’s little interest in the diamond sector from an equity perspective. I don’t see how in a potential IPO there’s enough interest in a new diamond story,” he said. “This has to be a private sale or consortium that needs to come in and take a longer-term view of the diamond sector. There could be growth expected in the retail segment. That’s where I think anyone taking a look at De Beers would see the value.”

Both analysts also see the De Beers sale having minimal impact on the junior exploration sector for diamonds.

“In order to stimulate exploration across the industry you would have to see a notable diamond price recovery,” Zimnisky said. “Prices have been flat for almost a decade now.”

De Beers has launched an ambitious five-year plan to become the premier jewelry brand worldwide, Diamond World reports.

CEO Al Cook aims to expand De Beers’ retail presence to compete with luxury giants like Tiffany and Cartier. Cook envisions transforming De Beers from a mining-focused company into a leading jewelry house, capitalizing on its rich legacy and market influence.

In an interview with the Financial Times, Cook said: “Diamonds’ future extends far beyond mining. I’m thrilled by the potential to execute our comprehensive strategy, aspiring to establish the world’s most prestigious jewelry maison—a vision that transcends traditional mining company boundaries.”

Central to this transformation is De Beers’ “Origins” strategy, which seeks to drive demand for mined diamonds by appealing to a new generation of consumers. This includes revitalizing marketing efforts and using innovative techniques to enhance the brand’s reach.

A key part of De Beers’ strategy is strengthening relationships with retail partners. Future plans include forming strategic alliances with major retailers, such as Signet Jewelers in the United States and Chow Tai Fook in China.

The Botswana government may raise its shareholding in global diamond miner De Beers, President Mokgweetsi Masisi told JCK News, after parent company Anglo American said it plans to spin off or sell the business.

The government owns a 15% stake in De Beers and Botswana accounts for 70% of the company’s annual rough diamond supply.

Anglo outlined a radical review of its business including a sale or divestment of the diamond business to focus on copper, iron ore and a fertilizer project in the UK to fend off a takeover from bigger rival BHP Group.

Masisi told JCK in Las Vegas that Anglo’s sale of De Beers would be “the best thing” if it happens.

The government could raise its shareholding in De Beers “if it’s attractive to,” Masisi told the online diamond news channel. The president in May told CNBC Africa that government would defend its interests in the diamond miner.

Among the plans Anglo could consider is an initial public offering for the diamond business, Reuters reported on May 14, citing sources.

Like other luxury goods, diamond prices have been hammered by a slump in global demand. De Beers has been limiting supply and offering flexibility to contracted customers. In February, Anglo announced a $1.6 billion impairment charge on De Beers. Anglo acquired De Beers in 2011, buying the Oppenheimer family’s 40% stake for $5.1 billion.

Masisi told JCK News Botswana’s ideal partner in De Beers would be a long-term investor. The government will try to keep the “bad guys out” and wants investors whose vision is aligned with the government’s.

“One of the characteristics of a bad owner is someone who has impatient capital,” Masisi said. “This industry requires somebody who is in it for the long-haul, because it has its ups and downs.”