Luxury Diamond Jewellery Trends for 2026, The Return of Quality, Individuality and Timeless Style

For years, fashion dictated what jewellery people wore. In 2026, that has changed. Today’s luxury jewellery buyers[…]

Diamond Setting Styles: Beauty, Light Performance and Security – Choosing the Right Setting for Every Gem

When most people admire a beautiful diamond ring, they naturally focus on the gemstone itself. Yet one[…]

Buying Jewellery for Babies and Young Children: What Every Parent and Grandparent Should Know

Giving a piece of jewellery to a newborn or young child is a tradition that has been[…]

Men’s Jewellery: From Kings and Warriors to Everyday Style

For thousands of years, jewellery has been a symbol of power, wealth, achievement and identity.

How Do I Know Which Engagement Ring Style Is Right for Me?

An engagement ring is one of the most meaningful purchases you will ever make. It symbolises love,[…]

From an $18 Billion Giant to a $1 Billion Sale: The Rise and Reinvention of De Beers

De beers The Company That Built the Modern Diamond Industry

The Hidden Light Within Diamonds: How Fluorescence Can Enhance Beauty, Character and Value

Fluorescence occurs when a diamond is exposed to ultraviolet (UV) light. Invisible ultraviolet rays excite trace structural[…]

The Art of Contrast: Why Mixing Coloured Diamonds Creates Extraordinary Jewellery

For centuries, white diamonds have been regarded as the ultimate symbol of elegance and timeless beauty. Today,[…]

Choosing the Perfect Diamond Shape for Your Hand: A Guide to Finding the Most Flattering Ring

Selecting a diamond is about far more than choosing the largest stone or the most popular shape.[…]

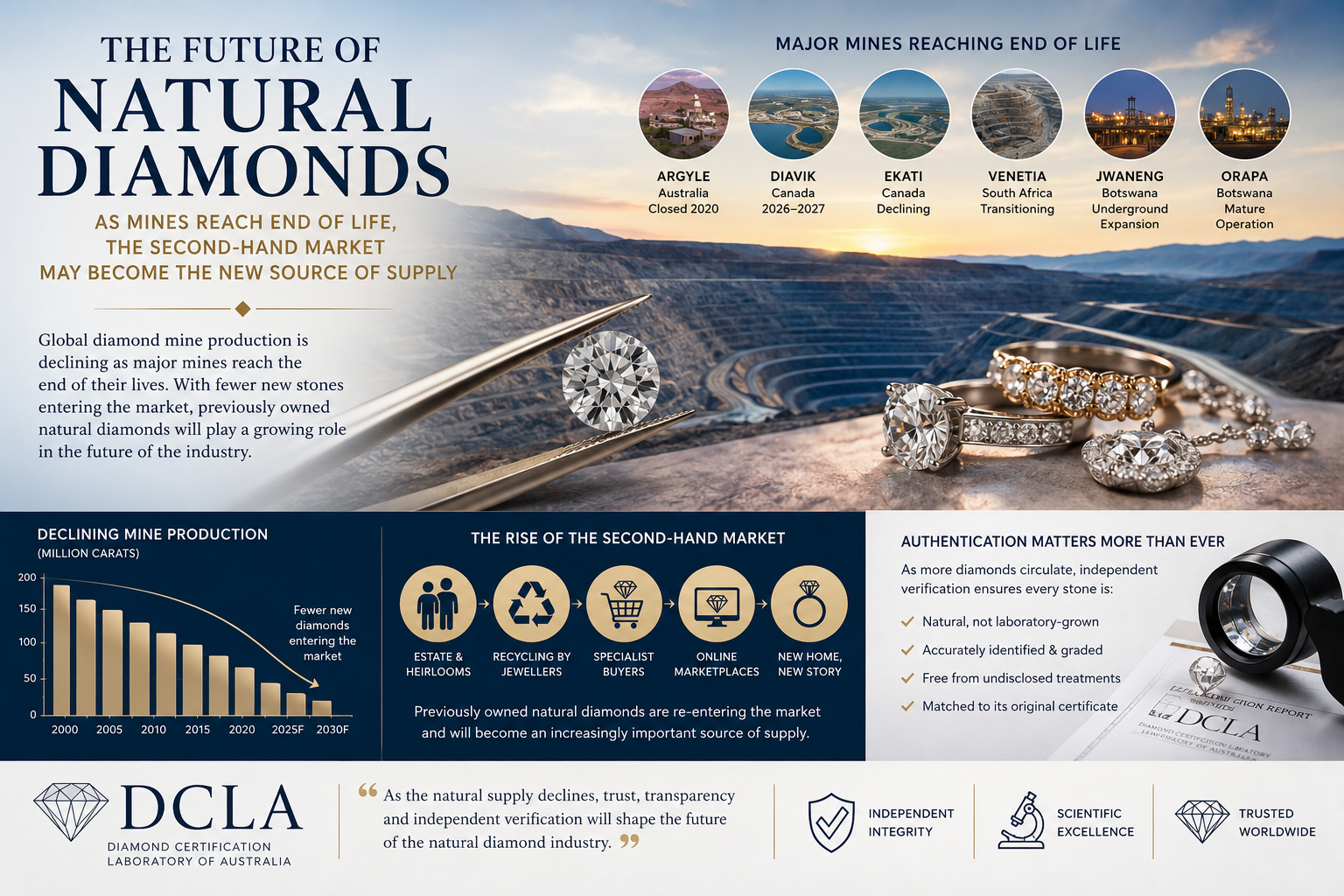

The Future of Natural Diamonds: As Global Mines Reach End of Life, Will the Second-Hand Market Become the New Source of Supply?

New Discoveries Are Becoming Increasingly Rare Diamond exploration is an expensive, high-risk undertaking. Unlike previous decades, when rich kimberlite[…]