It can be challenging to determine the exact location where a diamond was mined, but there are several ways to get an idea of its origin:

Diamond certificate: A diamond certificate or grading report from a reputable laboratory such as GIA, AGS, HRD, IGI or DCLA will provide information about the diamond’s characteristics, including its colour, clarity, and carat weight. Some certificates may also include information about the diamond’s origin or a statement that the diamond is of natural origin.

Inscription: Some diamonds may have a laser inscription on the girdle (the thin outer edge) of the diamond that identifies the diamond’s report and sometimes brand origin or other information about the diamond. The inscription is a laser inscription or a micro-inscription that can only be viewed under magnification.

Jewellers and diamond dealers: An experienced jeweller or diamond dealer may be able to provide information about the diamond’s origin based on their knowledge and experience in the industry.

Diamond tracing programs: Some diamond companies offer programs that trace the origin of their diamonds from the mine to the consumer. For example, the De Beers Group has a program called Tracr that provides a digital certificate of a diamond’s journey from mine to retailer. It’s important to note that not all diamonds can be traced to their exact origin, but the above methods can provide some information about a diamond’s potential source.

Diamonds can be found in various places around the world, but the most famous diamond sources are:

Botswana: Botswana is the world’s leading producer of diamonds by value and is responsible for about 25% of the world’s diamond supply.

Russia: Russia is the world’s largest diamond producer by volume, accounting for about 27% of global diamond production. The majority of diamonds mined in Russia come from the Yakutia region in northeastern Russia.

Canada: Canada is the world’s third-largest diamond producer, and its diamond mines are known for producing high-quality gemstones. The majority of Canada’s diamond mines are located in the Northwest Territories.

Australia: Australia is known for producing some of the world’s most valuable pink and red diamonds. The Argyle Diamond Mine in Western Australia was the world’s largest source of pink diamonds until its closure in 2020.

South Africa: South Africa is one of the earliest sources of diamonds, and the country’s Kimberley region is famous for its diamond mines. The Cullinan Diamond, the largest rough diamond ever found, was discovered in South Africa in 1905.

HRD Antwerp has sued its former Turkish partner company following allegations the Belgian laboratory had routinely “upgraded” diamonds.

The organization is in a dispute with Enstitü Istanbul Bilim Akademisi Yönetim Danışmanlığı, with which it ended a longstanding collaboration in 2021.

The messy divorce intensified last week when the Belgian press reported allegations that HRD, in 2020, had introduced a strategy of giving diamonds higher grades than other laboratories. On Wednesday, HRD said it had taken legal action against its former partners in Turkey for “damaging its business reputation.”

Belgian lawsuit

The disagreement revolves around a civil lawsuit that Enstitü Istanbul Bilim Akademisi Yönetim Danışmanlığı filed in late 2021 against HRD at an Antwerp court, according to a March 9 report by Belgian newspaper De Tijd. Investigators have also been looking into whether there was anything suspicious about the HRD’s grading methods, the report added.

Nearly six years ago, according to De Tijd, the International Diamond Council (IDC) — which the World Federation of Diamond Bourses (WFDB) set up in the 1970s to unify diamond grading around the world — excluded HRD from its membership. In a letter to HRD’s then CEO Michel Janssens, IDC president Harry Levy wrote that it was “no longer the case” that HRD graded according to IDC rules, the newspaper reported.

By then, HRD was in a bad financial state, according to leaked internal slides that the newspaper cited. This was still the case in 2020, when another leaked document read: “With current results, HRD is out of business,” the Dutch-language report said.

In a new strategy, HRD determined that stones that already had Gemological Institute of America (GIA) reports were allowed to receive one or two color “upgrades” or one clarity “upgrade,” the report alleged. The lab was not to downgrade the diamonds unless there had been a genuine mistake, the report continued. Stones from IGI were not allowed to receive an upgrade, it said. The paper cited an internal online meeting in which Mike Davey, then director of HRD Antwerp Istanbul, shot down the policy as a “way to commit market fraud.”

In the same meeting, HRD Istanbul owner Mehmet Can Özdemir said, according to the report: “Valuing diamonds involves a certain amount of subjectivity. If things are really tight, graders can go higher or lower. But that is never about one full degree. In our scenario, we immediately jump up two.”

HRD performed an audit of its standards following the allegations and found no irregularities, its CEO, Ellen Joncheere, told Rapaport News Wednesday.

“We are in fact a bit more lenient [than the GIA] on color but stricter on cut and fluorescence, but this is known by the market,” Joncheere said.

Trademark disagreement

On Wednesday, HRD also responded with allegations that Özdemir had “made shady deals” and had used HRD’s power and reputation unfairly.

“One of the main reasons for the termination [of the partnership] was that the partners holding the management of the company did not transfer the trademark ‘HRD,’ which was unfairly registered in the name of HRD Istanbul, to the clients [HRD Antwerp], despite their previous commitments,” said Tuncay Çaltekin, HRD Antwerp’s attorney, in a statement Wednesday.

The partners also placed liens on the HRD trademark through other companies owned by their family members and transferred HRD’s assets into those companies, Çaltekin alleged. “In other words, they committed irregularities contrary to the agreement,” he claimed.

Meanwhile, Joncheere gave an interview to Belgian newspaper Het Laatste Nieuws (HLN), published Wednesday, in which she alleged there had been “tax and financial fraud” at the Turkish counterpart.

Özdemir dismissed the CEO’s claims as “pathetic, dishonest and desperate.”

De Beers’ sales fell at its February trading session as sightholders deferred demand to later in the year amid uncertain market conditions.

The second sales cycle of 2023 grossed $495 million, a drop of 24% from last year’s equivalent period, the company reported Wednesday. Sales were, however, 9% higher than January’s $454 million.

“We know that sightholders planned more of their purchases for later in 2023, given the economic uncertainty at the time they were taking their planning decisions at the end of 2022,” said Al Cook, De Beers’ new CEO. “It is also encouraging to see some positive trends in end-client demand for diamond jewelry at the start of the year.”

The total includes the company’s February sight as well as auctions. The company raised prices of its smallest diamonds for the contract sale, but mostly maintained rates for larger stones after January’s price decline, customers told Rapaport News.

De Beers’ rough revenues have fallen 28% year on year to $949 million for the first two sales cycles of 2023, according to Rapaport calculations based on the company’s sight reports.

As of 2021 the laboratory-grown diamond trade market was estimated to be worth around $1.9 billion, according to a report by Frost & Sullivan.

This market is expected to grow significantly in the coming years, with some estimates suggesting that it could reach a value of over $15 billion by 2035.

laboratory-grown diamond trade has been growing steadily in recent years. There are several factors driving this growth.

Price: Laboratory-grown diamonds are typically less expensive than natural diamonds, which makes them an attractive option for consumers who are looking for high-quality jewelry at a more affordable price.

Ethical concerns: Some consumers are hesitant to purchase natural diamonds due to concerns about ethical issues such as conflict diamonds. Laboratory-grown diamonds are considered to be a more ethical alternative, as they are produced in a controlled environment and do not have the same potential ethical issues as natural diamonds.

Environmental concerns: The process of mining natural diamonds can have a significant environmental impact. Laboratory-grown diamonds are generally considered to be more environmentally friendly, as they do not require mining.

Advancements in technology: The technology used to produce laboratory-grown diamonds has improved significantly in recent years, making it easier and more cost-effective to produce high-quality diamonds. All of these factors have contributed to the growth of the laboratory-grown diamond trade, and it is expected to continue to grow in the coming years.

The answer is not yet: It is worth noting that natural diamonds still hold a significant share of the diamond market, and it remains to be seen how much of an impact laboratory-grown diamonds will have on the industry as a whole over the next decade.

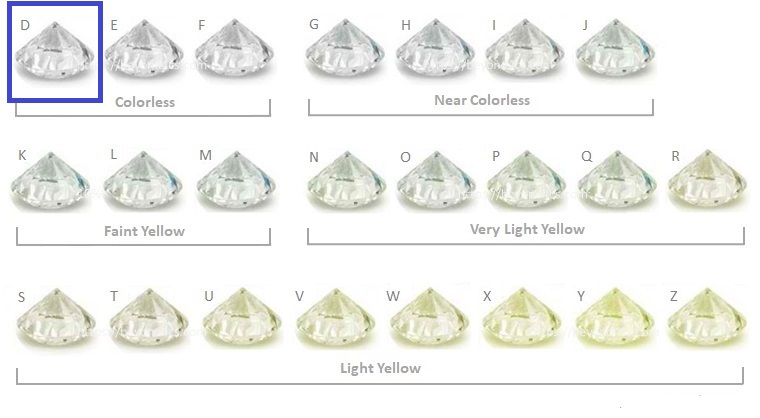

Diamond Colour is one of the 4c’s used to calculated diamond value

Polished diamond prices are derived from a variety of factors, including supply and demand, the quality and characteristics of the individual diamond, and market conditions.

The prices of polished diamonds are primarily determined by the 4Cs: carat weight, colour, clarity, and cut. These factors are assessed by gemologists and other experts who evaluate the diamond’s physical properties, such as its size, colour, clarity, and overall quality of cut.

Other factors that may influence the price of polished diamonds include the type of diamond, such as whether it is a natural or lab-grown diamond, the country of origin, and the overall market conditions for diamonds. Additionally, the reputation and credibility of the seller or the dealer can also affect the price of the polished diamond.

Overall, polished diamond prices are determined by a complex combination of factors, and can fluctuate over time based on changes in supply and demand, market conditions, and other economic and industry factors. There is no single diamond price list that accurately reflects the prices of all diamonds. This is because the price of a diamond depends on a number of factors, including its size, shape, colour, clarity, and other characteristics.

That being said, there are various industry-standard diamond price lists that are commonly used as references by professionals in the diamond trade. These lists are typically based on a standardized grading system and provide price ranges for diamonds of different sizes, shapes, and quality grades.

The most commonly used diamond price list is the Rapaport Diamond Report, which provides a benchmark price for diamonds based on their 4Cs grading (carat weight, colour, clarity, and cut). However, it is important to note that the Rapaport price list only reflects the wholesale price of diamonds and may not necessarily reflect the retail price that consumers will pay.

Other diamond price lists include the International Diamond Exchange Price List, the Idex Diamond Price Report, and the Polished Prices Diamond Index, among others. These price lists may differ in their methodologies and grading systems, and the prices they list may vary slightly from one another.

Ultimately, when buying or selling a diamond, it is important to work with a reputable and knowledgeable diamond professional who can help you evaluate the diamond’s characteristics and provide you with an accurate price estimate based on current market conditions. Source: Michael Cohen DCLA

Diamond traceability refers to the ability to track the journey of a diamond from its source to the market. This includes tracing the diamond’s origin, the path it takes through the supply chain, and the ultimate destination where it is sold to consumers.

Diamond traceability is important for a number of reasons. For one, it can help ensure the ethical and sustainable sourcing of diamonds, by allowing for greater transparency and accountability in the supply chain. This can help prevent the trade of conflict diamonds, which are used to finance armed conflict and human rights abuses. Additionally, diamond traceability can help provide assurance to consumers that the diamonds they purchase are of high quality and have been sourced responsibly.

The diamond industry has established various initiatives to promote diamond traceability, including the Kimberley Process Certification Scheme, which aims to prevent the trade of conflict diamonds, and the Responsible Jewellery Council, which sets standards for responsible sourcing practices in the industry. Additionally, some diamond producers have implemented blockchain technology to enable the secure tracking of diamonds throughout the supply chain.

Certification is another key aspect of diamond traceability. By obtaining a diamond certificate, which includes a record of the diamond’s characteristics and its journey through the supply chain, consumers can be assured that the diamond they are purchasing is of high quality and has been sourced responsibly. Overall, diamond traceability is an important aspect of the diamond industry, as it can help promote responsible sourcing practices and provide assurance to consumers about the quality and authenticity of the diamonds they purchase.

While it may not be possible for an individual to physically track a diamond from the source, certification and other industry initiatives can help ensure the ethical and sustainable sourcing of diamonds, as well as provide assurance to consumers about the quality and authenticity of the diamonds they purchase.

One technique used to determine the origin of diamonds is through the analysis of their chemical composition. Diamonds from different geographic locations can have different trace elements and isotopic compositions, which can be used to identify their origin. For example, diamonds from different mines in South Africa can have different isotopic signatures.

Another method to determine the origin of a diamond is through the use of spectroscopy, which involves analyzing the unique spectral characteristics of a diamond. This can provide clues about its origin and the geological conditions under which it formed.

It’s worth noting that while these techniques can provide clues about a diamond’s origin, they are not foolproof and may not provide a definitive answer in every case. Nonetheless, advances in technology and the diamond industry’s commitment to responsible sourcing have made it increasingly possible to track and trace diamonds from their source.

Conflict diamonds, also known as blood diamonds, are diamonds that have been mined in war zones and sold to finance armed conflict against governments. These diamonds are typically mined under inhumane conditions by workers who are often forced to work in dangerous and exploitative conditions. The profits from the sale of these diamonds are then used to fund armed conflicts, which often involve violence, human rights abuses, and forced labor. This cycle of violence and exploitation is known as the “diamond curse.” To combat the trade in conflict diamonds, the international community has established the Kimberley Process Certification Scheme, which requires that all rough diamonds be certified as conflict-free before they can be sold on the international market. The Kimberley Process has helped to significantly reduce the trade in conflict diamonds, but concerns remain about the effectiveness of the scheme and the ongoing trade in illicit diamonds.

What percentage of diamond production are conflict diamonds The percentage of diamond production that can be considered conflict or blood diamonds has decreased significantly since the introduction of the Kimberley Process Certification Scheme in 2003. According to the Kimberley Process, the percentage of conflict diamonds in the global diamond trade has fallen from approximately 15% in the 1990s to less than 1% today. However, it is important to note that some critics have raised concerns about the effectiveness of the Kimberley Process in preventing the trade in conflict diamonds. They argue that the definition of conflict diamonds used by the Kimberley Process is too narrow, and that some diamonds mined in areas of conflict may still be entering the market through illegal channels. Furthermore, there have been reports of human rights abuses and unethical practices in diamond mining in countries that are not considered conflict zones. So while the percentage of conflict diamonds in the global diamond trade is believed to be low, it is important to remain vigilant and continue efforts to ensure that all diamonds are mined and traded ethically and responsibly.

How do i ensure the diamond i buy is conflict free To ensure that the diamond you buy is conflict-free, you should look for a diamond that has been certified as such by a reputable organization. The most widely recognized certification scheme for conflict-free diamonds is the Kimberley Process Certification Scheme (KPCS), which was established in 2003 to prevent the trade in conflict diamonds. Here are some steps you can take to ensure that the diamond you buy is conflict-free:

Buy from a reputable jeweller: Look for a jeweller that is committed to selling conflict-free diamonds and has a policy in place to verify the origin of their diamonds. Many jewelers are members of organizations that promote ethical and responsible diamond sourcing, such as the Responsible Jewellery Council or the Jewelers of America.

Ask for a certificate of authenticity: Ask your jeweller for a certificate of authenticity that verifies the origin of the diamond you are interested in buying. The certificate should state that the diamond is conflict-free and has been mined and traded in compliance with the Kimberley Process.

Look for laser inscriptions: Some diamonds may have a laser inscription on the girdle that indicates the origin of the diamond and its certification number. This can be a helpful way to verify the diamond’s origin and ensure that it is conflict-free.

Consider buying a lab-grown diamond: Lab-grown diamonds are an ethical and sustainable alternative to mined diamonds. They are produced in a laboratory using advanced technology and do not have the same environmental or social impacts as mined diamonds.

By taking these steps, you can help ensure that the diamond you buy is conflict-free and has been mined and traded in a responsible and ethical manner.

Argyle pink diamonds are extremely rare and highly sought-after, making them some of the most valuable diamonds in the world. The Argyle diamond mine in Western Australia is the primary source of pink diamonds, and it is estimated that only 0.01% of the diamonds recovered from the mine are pink in colour, with an even smaller percentage being of the highest quality.

The Argyle mine ceased operations in 2020, which has led to speculation that the prices of pink diamonds, including argyle pink diamonds, may increase in the coming years. With the mine no longer producing new stones, the limited supply of these rare diamonds is expected to drive up demand and prices. However, like any investment, it’s important to carefully consider market trends and consult with a qualified professional before making any decisions.

The largest pink argyle diamond found to date is the Argyle Pink Jubilee, which was discovered at the Argyle mine in Western Australia in 2011. The diamond weighs 12.76 carats and is a vivid pink colour, making it one of the largest and most valuable pink diamonds ever found. The Pink Jubilee was cut and polished over a period of ten months, during which time the rough diamond was studied and analyzed extensively to determine the best way to bring out its natural beauty and maximize its value. The diamond was sold at auction in 2013 for an undisclosed sum, but it is believed to have fetched a record-breaking price per carat for a pink diamond.

Red diamonds are extremely rare, even more so than pink diamonds. It is estimated that only a handful of natural red diamonds are found each year, and most of them are less than half a carat in size. Red diamonds are so rare that many jewelers and gemologists may go their entire careers without ever seeing one.

The red colour in diamonds is caused by the presence of a rare mineral which causes “graining,”, This occurs when the crystal structure of the diamond is distorted during its formation. The graining causes the diamond to absorb green light and reflect red light, resulting in a beautiful and distinctive red hue. Because of their rarity, red diamonds are among the most valuable and expensive gemstones in the world. They are highly sought-after by collectors and investors, and prices for top-quality stones can reach millions of dollars per carat at auction.

Blue diamonds are also quite rare, but not as rare as pink or red diamonds. Blue diamonds account for only about 0.02% of all diamonds mined worldwide. The blue colour in diamonds is caused by the presence of trace amounts of boron during their formation, which causes the diamond to absorb red, yellow, and green light, resulting in a blue hue.

Blue diamonds are highly prized for their unique colour and rarity, and they can command very high prices at auction. The value of a blue diamond depends on a variety of factors, including its size, colour intensity, clarity, and overall quality. Blue diamonds range in colour from pale blue to vivid blue, with the most valuable stones being those with a deep, rich blue colour.

One of the most famous blue diamonds is the Hope Diamond, which is a 45.52-carat blue diamond that is part of the Smithsonian Institution’s collection of natural history specimens.

The most expensive diamond ever sold is the Pink Star, a 59.60-carat oval-cut pink diamond that was sold for $71.2 million at a Sotheby’s auction in Hong Kong in 2017. The diamond, which is the largest internally flawless fancy vivid pink diamond ever graded by the Gemological Institute of America (GIA), was mined in Africa in 1999 and took two years to cut and polish.

The Pink Star was originally sold at auction in 2013 for a record-breaking $83 million, but the sale was later cancelled after the buyer defaulted on the payment. The diamond was put back up for auction in 2017 and sold to a jewelry retailer in Hong Kong for $71.2 million, setting a new world record for the most expensive diamond ever sold at auction.

Yellow diamonds are not as rare as pink, red, or blue diamonds, but they are still considered rare and highly prized. Yellow diamonds are formed when nitrogen atoms are trapped in the crystal lattice structure of the diamond during its formation, causing it to absorb blue light and reflect yellow light.

The intensity of the yellow colour in a diamond can vary widely, ranging from a pale yellow or light lemon colour to a deep, intense yellow. The most valuable yellow diamonds are those with a deep, rich colour that is evenly distributed throughout the stone.

Yellow diamonds are mined in various parts of the world, including South Africa, Australia, and Canada. While yellow diamonds are not as rare as some other coloured diamonds, high-quality yellow diamonds can still command very high prices at auction, especially those with a large carat weight and intense colour.

Orange diamonds are considered rare and highly valuable. The orange colour in diamonds is caused by the presence of nitrogen and other impurities in the crystal lattice structure of the diamond, which absorb blue and green light, resulting in an orange hue.

Orange diamonds can range in colour from pale orange to a deep, vivid orange, with the most valuable stones being those with a pure and intense colour. Orange diamonds are not as commonly found as white or yellow diamonds and are considered much rarer than brown or gray diamonds.

The most famous orange diamond is the Pumpkin Diamond, a 5.54-carat fancy vivid orange diamond that was mined in South Africa. The Pumpkin Diamond was sold at auction in 1997 for over $1.3 million, and it is now part of the collection at the Smithsonian Institution’s National Museum of Natural History in Washington, D.C.

De Beers has increased prices of small rough diamonds for the second consecutive sight as a combination of demand and supply factors continue to create a hot market for the category.

Prices for tiny stones rose by around 10% on average at this week’s trading session, with sharper advances in certain segments, customers and insiders estimated Monday. The changes were mainly for minus-7 sieve sizes, which weigh about 0.03 carats, across a range of qualities. De Beers was unavailable for comment.

The February sale runs this week from Monday to Friday in Gaborone, Botswana.

Rough under 0.75 carats became a sought-after asset in the second half of 2022 as melee demand from luxury brands strengthened and Indian manufacturers needed cheaper material to fill factories amid thin profit margins. In addition, Western sanctions on Russian diamonds created a mixture of real and perceived shortages in those sizes, for which Alrosa is the biggest supplier. The trade is watching for potential further restrictions as the one-year anniversary of Russia’s invasion of Ukraine approaches.

“Are people preempting what the [new] measures might be on Russia? [The strong market] might have to do with that,” a rough-market participant told Rapaport News on condition of anonymity.

Last year, De Beers made only modest increases in the prices of smalls, even when the segment saw robust demand, a sightholder explained on condition of anonymity. The miner raised prices at last month’s sight by approximately 10% — alongside decreases in the slower, larger goods.

The fresh hikes caught many dealers by surprise, as they were expecting De Beers to monitor the Chinese recovery before making further price adjustments.

Botswana’s President Mokgweetsi Masisi warned Sunday that his country could sever ties with South African diamond giant De Beers if talks to renegotiate a sales agreement prove unfavorable for his country.

The 2011 sales agreement governing the terms of marketing diamonds produced by Debswana – a 50-50 joint venture between the government and De Beers – expired in 2021.

It has been extended by the parties, who cited the coronavirus outbreak as the reason for the delay in concluding negotiations, and will end on June 30, 2023.

Speaking at a rally of his ruling Botswana Democratic Party (BDP) in his home village of Moshupa, about 65 kilometers from the capital Gaborone, Masisi warned, “If we don’t reach a win-win situation, each side will have to pack up and go home.”

Under the 2011 agreement, the mining company De Beers received 90% of the rough diamonds produced while Botswana, Africa’s largest diamond producer, received 10%. In 2020, Botswana’s share was increased to 25%.

In 2020, Botswana’s share was increased to 25%.

Today, “we got a glimpse of how the diamond market works, and we found out that we received less than we should have,” said Mr. Masisi, who spoke in both English and the local language, Tswana.

“We also found out that our diamonds are bringing in a lot of profit and that the (2011) agreement had not been favorable to us,” he added, before warning: “We want a bigger share of our diamonds. Business cannot continue as before.