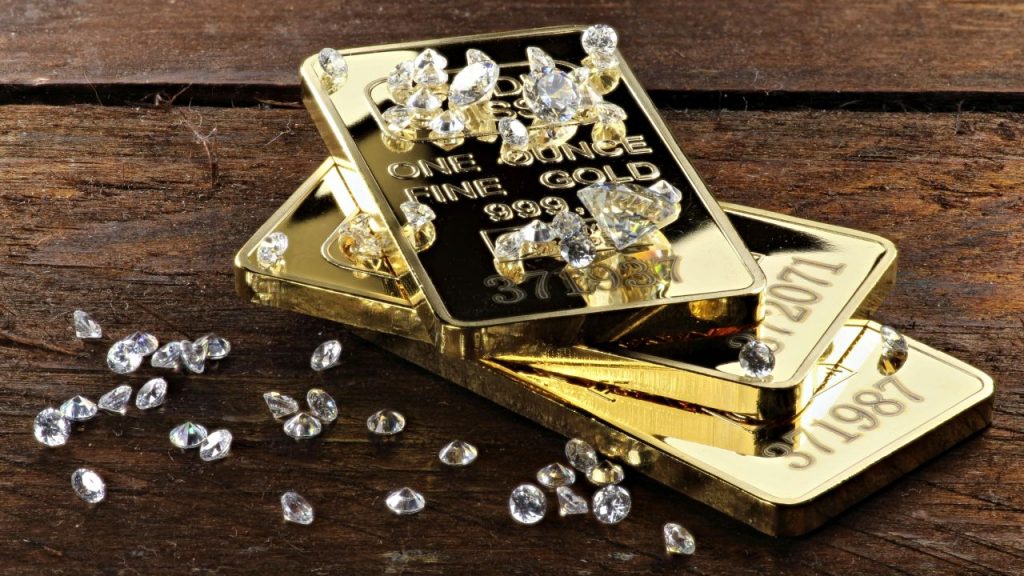

Cryptocurrency mogul Richard Heart allegedly used proceeds from the sale of unregistered securities to buy the 555-carat Enigma diamond, according to the US Securities and Exchange Commission (SEC).

The SEC has charged Heart — who was born Richard Schueler and who created the Hex cryptocurrency token — with selling the securities to raise more than $1 billion from investors. It alleges that Heart and his PulseChain company committed fraud by misappropriating at least $12 million of those funds to purchase luxury items, including sports cars, watches and the diamond.

“Heart called on investors to buy crypto asset securities in offerings that he failed to register,” Eric Werner, director of the SEC’s Fort Worth regional office, said in a statement Monday. “He then defrauded those investors by spending some of their crypto assets on exorbitant luxury goods.”

The Enigma, which is believed to have come from outer space, is the largest faceted diamond of any kind to appear at auction. Heart purchased it from Sotheby’s at a one-off sale in February 2022 for GBP 3.2 million ($4.3 million). At the time, Heart tweeted that he had bought the stone and would rename it the Hex.com diamond as a nod to his cryptocurrency platform, calling it a “match made in heaven.” Hex has a “5555 day club” comprising people who hold 5,555-day Hex stakes — the longest possible stake in the electronic token.

Sotheby’s, which accepted payment for the Enigma, was not mentioned as a defendant in the SEC’s lawsuit.

“Sotheby’s does not comment on individual transactions, but we can confirm we have established due diligence procedures, tailored and updated to take account of our requirements to conduct business in compliance with applicable laws and regulations,” the auction house stated.

The US Department of the Treasury has issued sanctions against four companies and an individual in the gold and diamond industries that have provided funding to Russian military organization Wagner Group.

The Central African Republic (CAR), United Arab Emirates (UAE) and Russia-based entities have “engaged in illicit gold dealings” to help Wagner “sustain and expand” its army in Ukraine and Africa, the government office said Tuesday.

“Treasury’s sanctions disrupt key actors in the Wagner Group’s financial network and international structure,” explained Brian Nelson, under secretary of the Treasury for Terrorism and Financial Intelligence. “The Wagner Group funds its brutal operations in part by exploiting natural resources in countries like CAR and Mali.”

The targets include:

Midas Ressources, which holds the rights to the Ndassima gold mine in CAR, and Diamville, a gold and diamond purchasing company that participated in a gold scheme and the shipment of diamonds mined in the African country to help fund Wagner activities. Dubai-based industrial goods distributor Industrial Resources General Trading, which provided support to Wagner leader Yevgeniy Prigozhin by purchasing the diamonds sold by Diamville in exchange for cash to support the military group. Limited Liability Company DM (OOO DM), a Russia-based firm accused of participating in a gold-selling scheme with Diamville. Andrey Ivanov, an executive in the Wagner Group who facilitated weapons deals and mining operations with the government of Mali. The announcement follows Wagner’s attempted rebellion against the Russian government last week. Prigozhin called off the mutiny and went into exile in Belarus.

The sanctions are the latest round against the Wagner Group, which the US has labeled a “significant transnational criminal organization.” Australia, Canada, Japan, the UK and the European Union have also sanctioned the military entity.

De Beers’ sales value fell this month as global rough demand weakened and the miner reduced prices of its larger stones.

Proceeds dropped 32% year on year to $450 million at 2023’s fifth sales cycle from $657 million in the equivalent period a year earlier, De Beers reported Wednesday. Sales declined 6% compared with the $479 million that the fourth cycle brought in. The total included the June sight as well as auction sales.

“Following the JCK [Las Vegas] show, and with ongoing global macroeconomic challenges continuing to impact end-client sentiment, the diamond industry remains cautious heading into summer,” said De Beers CEO Al Cook. “Reflecting this, we saw demand for De Beers rough diamonds during the fifth sales cycle of the year slightly softer than in the fourth cycle.”

De Beers lowered prices at the sight by 5% to 10% mainly in 2-carat categories and larger, as well as for some 1- to 1.5-carat items, market insiders said. It also extended its buyback program, which allows sightholders to sell goods back to the miner following the purchase.

This reflected weakness in the rough that produces polished above 0.30 carats, and especially the stones that yield 1-carat finished diamonds. These sizes are especially weak in the US market amid economic uncertainty and a lull in engagements, dealers explained. Rough under 0.75 carats has seen a mild recovery as Indian manufacturers look to fill their factories with low-cost material.

The Group of Seven (G7) meeting that took place in Japan in mid-May proved to be an anticlimax for the diamond trade.

The industry had expected a major announcement to come from the meeting relating to required declarations on the origin of diamonds imported to those countries — an additional measure that would help prevent polished diamonds sourced from Russian-origin rough entering their markets.

While a clear guideline did not emerge, the member nations — Canada, France, Germany, Italy, Japan, the United Kingdom and the United States — pledged to work toward such measures.

“In order to reduce the revenues that Russia extracts from the export of diamonds, we will continue to restrict the trade in and use of diamonds mined, processed or produced in Russia,” the group said after the meeting.

As it stands, the US and the UK have implemented bans on diamonds sourced directly from Russia. However, the sanctions don’t account for “substantial transformation,” and consequently the manufacturing center is regarded as the source. For example, diamonds polished in Belgium, India, Israel or the United Arab Emirates (UAE) from Russian rough can technically be imported to the US.

Implementing such detailed declarations is proving more complicated than originally thought. Creating such mechanisms will take time, as Feriel Zerouki, the De Beers executive who heads the World Diamond Council (WDC), said in a recent panel discussion at the JCK Las Vegas show in early June. These measures would apply to the entire industry, seemingly requiring a disclosure of origin for all diamonds at customs.

“How do we support the [sanctions] without paralyzing the industry and making it very cumbersome for natural diamonds to enter the G7 countries,” Zerouki challenged the Las Vegas audience.

Setting standards It’s a sensitive point for an already heavily audited industry, and for companies in each segment of the supply chain that would bear the added expense of verifying such information.

It’s also worth noting that the G7 cannot enact such requirements as a bloc. It will be left to each country to implement its own import rules. That said, there does at least seem to be an effort among those countries to apply some consistency in their systems. It was an open secret that members of various governments and industry bodies met in Las Vegas during the show to advance these discussions, which presumably covered a wide spectrum of industry-related issues.

Central to the talks must surely be the practicality of such declarations. What mechanisms are available to the industry that would facilitate traceability? And who verifies that these initiatives meet the required standards? And on what are those standards based?

The trade has at its disposal industry structures as well as company programs that tackle the challenge of traceability and source verification — although arguably nothing is foolproof.

The just completed Sotheby’s Magnificent Jewels sale in New York is the first auction to sell two items for more than $30 million.

The first is the “Estrela de Fura,” a 55.22-carat Mozambique ruby that sold for $34.8 million ($630,288 per carat), establishing a world record price for a ruby and any colored gemstone sold at auction. It is also the largest ruby to be sold at auction. Its pre-auction estimate was more than $30 million.

The finished ruby was cut and polished from a 101-carat rough discovered by Fura Gems, a colored gemstone mining and marketing company based in Dubai. It was unearthed at its ruby mine in Montepeuz, Mozambique, in July 2022. The company named the rough gem, Estrela de Fura (Star of Fura in Portuguese). Even in its rough, untouched state, the ruby “was considered by experts as an exceptional treasure of nature for its fluorescence, outstanding clarity and vivid red hue, known as ‘pigeon’s blood’ — a color traditionally associated only with Burmese rubies,” Sotheby’s said in a previous statement.

It’s rare for a mining company to cut and polish the gem and then sell it at auction. The usual route of recently found colored gems is to sell it to a company as a rough where they would cut and polish the gem, then it would sell it privately or at auction. However, Dev Shetty, founder and CEO of Fura Gems, chose to not only go on the auction route on his own, but to embark on a worldwide tour of the rare gem, promoting not only this stone, but rubies from Mozambique as equal to rubies from Burma, which has historically been considered the main source of the most sought-after rubies.

Quig Bruning, head of Sotheby’s Jewelry America, previously said the Estrela de Fura may signal a change of this perception.

“It is undoubtedly positioned to become the standard bearer for African rubies – and gemstones in general, bringing global awareness to their ability to be on par with, and even outshine, those from Burma,” Bruning said in a statement.

A 4.83 carat fancy vivid blue diamond ring sold for $8.8m at Christie’s Hong Kong as the Magnificent Jewels sale brought in a total of almost $60m.

The brilliant cut IF Type IIb gem (pictured) was surrounded by fancy-cut diamonds, in a gold setting. It sold between the low and high estimates of $7m to $10.2m.

The blue diamond led the sale, followed by two items which both sold for above their high estimates.

An octagonal step-cut 21.38 carat sapphire in a platinum ring set with tapered baguette cut diamonds sold for $4.5m (high estimate $2.3m).

And an 8.92 carats fancy vivid yellow orange pear modified brilliant cut diamond, in a platinum and gold ring, with pear brilliant-cut diamonds of 1.12 and 1.11 carat, sold for $4m (high estimate $3.8m).

G7 countries are imposing fresh sanctions against Russia to try to further hinder its war effort in Ukraine. “If the sanctions continue, then there will be a lot of uncertainty in the employment of one million workers,” said Vipul Shah, chairman of Gem & Jewellery Export Promotion Council (GJEPC).

A Swiss company claims it has developed technology that chemically profiles any diamond so it can identify the country – and even the specific mine – of origin.

Spacecode says it analyzes diamonds at a molecular level to determine where it was mined, so it doesn’t matter whether the stone has been registered earlier in the supply chain.

The company has been in talks with the G7 and EU nations about the possibility of using its technology to identify Russian diamonds.

“Our research started 10 years ago, but over the past three years we have developed a specific technology that identifies the provenance of any diamond,” said Pavlo Protopapa the company’s CEO.

“We are the first ever to hold such unique technology, which is a major game changer all along the diamond supply chain.”

“We plan to produce by the end of this year our initial units. By 2024, we will offer on a large scale to the global diamond and jewelry industries, a small easy-to-use device that will define the country of origin of rough and polished diamonds.”

Protopapa added that “in meetings with the G7 and the EU representatives, we have received enthusiastic interest. Within months, we will deliver a small, easy-to-use device that will identify Angolan, Botswanan, South-African and of course, any Russian diamonds. We will leave it for the politicians to decide what to do with it”.

Spacecode’s breakthrough technology analyzes the chemical composition of a diamond on a molecular level, and with Artificial Intelligence tools, creates a “chemical profile” of the run of the mine of a specific diamond mine.

The technology identifies not only the country of origin, but even the specific mine in which it was mined.

Spacecode’s diamond inventory management technology already tracks more than 25 million stones. The company has a team of 15 engineers and specialists, and over 300 clients. Its technology could be adopted by the G7 and the EU to impose effective sanctions on both rough and polished diamonds from Russia.

It could also be used by the Kimberley Process and other organizations, to end, for example, the export of Angolan diamonds through other African countries.

Diamonds have long been revered for their beauty, rarity, and association with luxury. However, traditional diamond mining comes with ethical concerns and environmental impacts. In recent years, laboratory-grown diamonds have emerged as an alternative, marketed as a sustainable and eco-friendly choice. This article explores whether laboratory-grown diamonds truly live up to their claims of sustainability and environmental friendliness.

The Process of Laboratory-Grown Diamonds: Laboratory-grown diamonds, also known as synthetic or cultured diamonds, are created in controlled environments using advanced technology. They are produced through two primary methods: High-Pressure High-Temperature (HPHT) and Chemical Vapor Deposition (CVD). Both methods involve replicating the natural conditions that cause diamond formation but in a shorter time frame.

Environmental Impact: a) Land Disruption: Traditional diamond mining often requires extensive land clearing and excavation, leading to habitat destruction and soil erosion. In contrast, laboratory-grown diamonds are produced in labs, eliminating the need for land disruption.

b) Energy Consumption: The production of laboratory-grown diamonds does require significant energy inputs, mainly in the form of electricity. However, advancements in technology have made the process more efficient, reducing energy requirements over time. Renewable energy sources can also be used to power these facilities, further minimizing their carbon footprint.

c) Water Usage: Traditional diamond mining can consume substantial amounts of water, contributing to local water scarcity and ecosystem degradation. Laboratory-grown diamond production generally requires significantly less water, making it a more environmentally friendly option.

d) Chemical Usage: While the production of laboratory-grown diamonds involves the use of chemicals, the industry is continually striving to reduce their environmental impact. Responsible manufacturers are working on developing greener chemical processes and minimizing the use of harmful substances.

Ethical Considerations: Traditional diamond mining has long been associated with human rights issues, including exploitative labor practices and conflicts (so-called “blood diamonds”). Laboratory-grown diamonds, on the other hand, offer a more transparent and traceable supply chain. Consumers can be confident that their diamonds are not contributing to human suffering or funding conflicts.

Long-Term Sustainability: a) Repurposing Waste: Laboratory-grown diamond production generates significantly less waste compared to mining. Additionally, by-products from the manufacturing process can be repurposed, further reducing the ecological impact.

b) Circular Economy: As laboratory-grown diamonds gain popularity, a potential future advantage lies in their ability to be recycled and repurposed. This aligns with the principles of a circular economy, where materials are reused rather than discarded.

Conclusion:

Laboratory-grown diamonds offer an alternative to traditional diamond mining that addresses many of the ethical and environmental concerns associated with the industry. While there are energy and chemical inputs involved, the overall impact is significantly reduced compared to mining. Furthermore, the transparency and traceability of laboratory-grown diamonds provide assurance to consumers seeking an ethical and sustainable choice.

As with any industry, continuous improvements are needed to enhance the sustainability of laboratory-grown diamond production. Manufacturers should prioritize the use of renewable energy, minimize chemical usage, and explore recycling options. By doing so, laboratory-grown diamonds can truly become a more sustainable and eco-friendly option, offering consumers the beauty and luxury they desire without compromising the environment or human rights.

Western countries’ attempts to interfere with Russian diamond exports may lead to disruption of supply chains, which runs counter to the interests of the industry as a whole, Dmitry Birichevsky, the head of the Russian Foreign Ministry’s economic cooperation department, told Sputnik.

“It is clear that the restrictive measures that are being developed, whatever they may be, risk disrupting established supply chains and thus inimical to the interests of the diamond industry as a whole. In this regard, Westerners are trying to provide a plausible pretext for their irresponsible actions, including on various international platforms,” Birichevsky said.

Russia is one of the largest diamond industry players, accounting for 30% of world production, the official noted.

“At the same time, Russian manufacturers are exceptionally responsible market participants, whose activities not only meet, but often exceed international standards and are in many ways a model for others,” Birichevsky said.

He noted that opponents should be aware that any attempts to prevent Russian diamond exports are non-market oriented.

“For our part, we consistently counter attempts to deliberately distort the foundations and principles of the relevant multilateral formats that determine the functioning of the global diamond market. It is encouraging that a vast majority of industry representatives share our approaches,” Birichevsky added.

Earlier this month, top US and European Commission officials met with diamond industry leaders to discuss ways to cut-off billions in revenue to Russia.

In February, the Group of Seven (G7) countries agreed to further sanction the Russian diamond industry in an attempt to slash Russian revenues amid Moscow’s special military operation in Ukraine. The G7 said in a joint statement that they would engage key partners on further measures on Russian diamonds, including rough and polished ones.

On Saturday, Polish Prime Minister Mateusz Morawiecki said he expected the European Union’s 11th package of sanctions to target Russian state nuclear corporation Rosatom and Russian diamonds.