Diamond giant De Beers is fully prepared for the expanded G7 restrictions on diamond imports from Russia, which took effect on September 1st. These restrictions now include diamonds weighing 0.5 carats and above, according to Rough&Polished.

De Beers stated that its customers will continue to provide proof of the origin of the diamonds they sell, even as the sanctions now cover rough diamonds weighing 0.5 carats and above, instead of 1 carat and above, as previously stipulated.

The company added that it welcomes the G7’s measures, which stand alongside the diamond industry and diamond-producing nations, aiming to trace the origin of diamonds. “De Beers fully supports the work being carried out by the G7 to prohibit the trade in Russian diamonds, and we are committed to working with the G7, the diamond industry, and our partner governments to ensure there is an effective system put in place,” said De Beers CEO Al Cook.

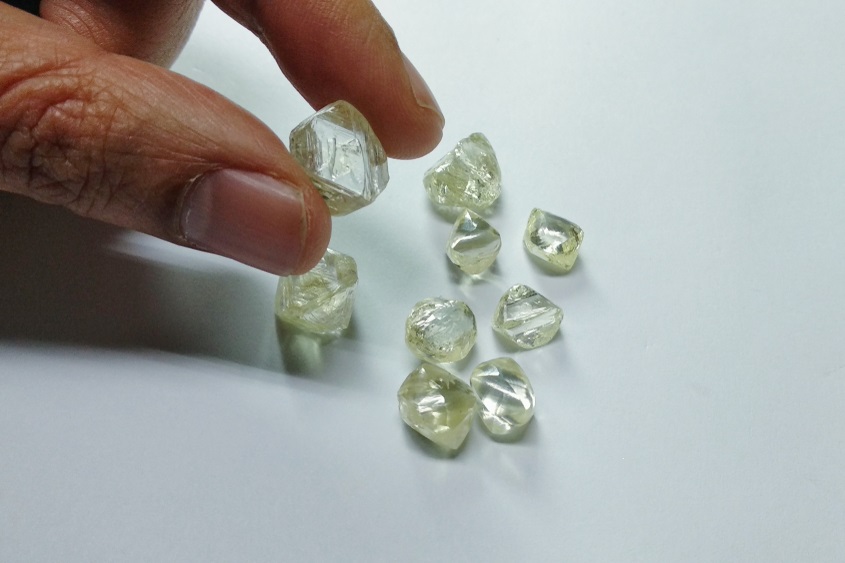

Africa-focused miner Gem Diamonds has unearthed yet another massive white diamond at its prolific Letšeng mine in Lesotho, just days after another major find.

The 122.2 carat Type II white diamond was recovered over the weekend and is the eleventh greater than 100-carat precious stone mined this year at the operation, the company said.

Sign Up for the Precious Metals Digest

Type IIa diamonds are the most valued and collectable precious gemstones, as they contain either very little or no nitrogen atoms in their crystal structure.

The Letšeng mine, owned 70% by Gem Diamonds, is one of the world’s ten largest diamond operations by revenue. At 3,100 metres (10,000 feet) above sea level, it is also one of the world’s most elevated diamond mines.

The operation has a track record of producing large, exceptional white diamonds, which makes it the highest-dollar-per-carat kimberlite diamond mine in the world.

The Perth Mint continues its Jewelled series of coins with a 10 ounce gold Jewelled Turtle coin with a mintage of eight coins.

And it comes with a price tag of $269,000 Australian ($182,229 U.S.).

This is the seventh release in the Jewelled series. It features a handset rare trademarked Argyle Pink Diamond and lustrous white diamonds that form the head and limbs of the three dimensional 18 karat gold turtle.

Each Jewelled Turtle coin is a Proof 10 ounce .9999 fine gold $2,500 denominated coin, with the centerpiece the 18-karat gold sea turtle surrounded by depictions of coral and dory fish.

The turtle’s head and limbs are embellished with 52 white diamonds, and two emeralds for its eyes. Additional white diamonds are set in a ribbon shaped line symbolizing the sea surface, with an Argyle Pink Diamond set at the heart of a stylized sun.

The Jewelled Series is developed each year in association with John Glajz, a Singapore based Argyle Pink Diamonds Icon Partner.

Each Jewelled Turtle coin is presented in a luxury display case adorned with 18 karat gold furnishings and inset with two Argyle Pink Diamond.

For the first time in the series, the coin bears the Dan Thorne effigy of King Charles III, as well as the P125 privy mark for the Perth Mint’s 125th anniversary.

Zimbabwe’s state-owned diamond company is forecasting a 16 per cent increase this year.

The Zimbabwe Consolidated Diamond Company (ZCDC) said it was ramping up production to 5.7m carats in 2024 and would aim to increase that figure to 10m carats next year.

Munashe Shava, ZCDC board chairman, said: “Commodity prices are depressed on the global market and we have come up with various initiatives to offset this worrisome development.

The Chronicle newspaper reported him as saying: “We have ramped up production and this year we have set a target of 5.7m carats and we see this target nearly doubling to 20m carats in the coming year.”

Zimbabwe, the world’s seventh biggest diamond producing nation, recorded an output of 4.9m carats, according to Kimberley Process data, valued at $303m. It exported 5.6m carats valued at $297m.

Earlier this year the US sanctioned Zimbabwe’s President Emmerson Mnangagwa for human rights abuses, corruption and smuggling gold and diamonds.

Mnangagwa, 81, who has held office since 2017, insists the claims against him are “defamatory” and “malicious”.

Australia-based jewelry retailer Michael Hill International reported a slight loss for FY 2024, amid “challenging” trading conditions.

Net profit after tax (NPAT) was minus AUD 479,000 (minus USD 322,000), compared to a positive AUD 35.2m (USD 22.5m) in FY 2023 and AUD 46.7m (USD 29.9m) in FY 20222.

The company has 300 stores in Australia, New Zealand and Canada, including low-price retailer Bevilles, Medley, and its new luxury business TenSevenSeven.

It reported increased revenues, up 4.2 per cent to AUD 644.9m (USD 437.4m), with Australia up 10.3 per cent, New Zealand down 11.8 per cent and Canada flat.

“While FY24 earnings were disappointing, with challenging economic conditions and inflationary pressures impacting consumers across all markets, the business continued to execute on its clearly articulated strategy, focus on retail fundamentals and drive topline sales,” said CEO Daniel Bracken, CEO and managing director.

He said it had been “a challenging and busy year”. The company noted in its FY 2024 Full Year Results that third-party data indicated it had continued to outperform the broader jewelry market.

Botswana’s state-owned diamond marketing company will increase its borrowing to fund additional rough purchases.

Finance Minister Peggy Serame said last Thursday (29 August) that the government had arranged a $300m credit facility, with the Standard Chartered Bank for the Okavango Diamond Company (ODC).

It hopes to capitalize on a long-awaited recovery the global diamond market.

At the moment ODC’s limited cash reserves mean it can only buy $70m of its allocation of diamonds produced by Debswana, the 50/50 joint venture between De Beers and the Botswana government.

ODC holds 10 auctions a year to sell its 25% allocation from Debswana. That share is set to double to 50 per cent over the next decade, as part of a deal agreed last year between Botswana and De Beers.

Last October ODC halted its rough sales amid weak demand.

Since early 2022, the price of polished natural diamonds has fallen approximately 40% and the industry is being buffeted by negative economic headwinds, an excess of mine supply and too much stock in the cutting centres. However, there is one statistic that cannot be ignored: around 50% of Diamond Engagement Rings purchased in the United States now contain a Lab Grown Diamond (LGD). Is this just another cyclical downturn or are we in the middle of a major structural change?

Diamonds were once the preserve of royalty and the uber-wealthy, but the diamond market has evolved over the past 80 years into more of a mass market product with democratisation of the diamond consumer. Since the late 1970s most polished diamonds below 5 carats were priced against the 4 ‘C’s’ (carat, clarity, colour and cut), which led to standardised pricing in the form of polished diamond pricing lists. Up until the turn of the century these lists were primarily available in the wholesale market, but the arrival of internet pricing soon gave the consumer access to that same standardised pricing. In a world where everyone knows the price of everything, branding is the only differentiator. Without a differentiator, commoditised products end up selling for the lowest price.

It was why one of the questions that De Beers tried to answer when it changed its business model 25 years ago was: “How do you take a necessity (the diamond) priced like a commodity and market it as a luxury priced like a brand?”

Unfortunately, that question remains unanswered. The industry did create hundreds of so-called ‘brands’; origin, cut, settings, etc; the problem was that very few of them were real “brands”. If something does not sell at a premium, it’s not a brand, and most natural diamonds sell at a discount, yet the more that the industry was unable to achieve a premium, the more it becomes fixated with talking about the “product” when the luxury world has spent the last 25 years talking about “values”.

The challenge for most jewellers is not making a sale, it is making a reasonable margin. Ask a jeweller what they are selling and if they reply “VS1, G-H colour, loose polished, 1-caraters” then the most relevant word in their business will be “discounting”, because what they are selling is a commoditised version of “crystallised carbon.” There is no differentiator.

The LGD industry realised that to succeed it simply needed to persuade consumers that natural diamonds and LGDs were the same – “optically, physically and chemically”, but to also position them as “slightly cheaper”. They could then ride on the back of 80 years of De Beers diamond advertising differentiate themselves by claiming that LGDs were “conflict free”.

A larger “ethical” LGD for the same money as a natural diamond or pay less for the same size, created a money printing machine for everyone involved. And it’s no surprise that LGDs real success has been in the United States, because historically America has always been a “discount market”, and “larger for less” plays to that tune.

If all you want in a diamond is the sparkle, then they are in essence the same. Except there is a very real difference between the two, which is why some LGD executives insist on calling natural diamonds “earth mined” diamonds, because “natural” is exactly what differentiates them. The story of their age, rarity, origin; their social and economic contribution but above all, their “social purpose”. It was the failure of the natural diamond industry to tell that story which opened the door to LGDs.

When LGD production exploded, wholesale prices collapsed to around a 95% to 98% discount to their natural diamond equivalent. Prices vary according to quality, but anecdotal evidence suggests that today in the wholesale market, it is possible to buy a single polished LGD for $150 a carat, buy in volume and its possible to pay as low as $80 a carat.

Many retailers have also dropped their LGD prices, but by no means as far, and even pricing LGD at a 20-40% discount to their natural diamond equivalent can still leave a very significant margin. Pandora will sell you a 1-carat LGD ring for $1,950. Helzberg Jewellers (a Warren Buffet company) will sell you a similar LGD for $1,999. It’s very likely that some in the LGD industry are making a gross margin of 200%, some much more for a product that Signet Jewellers sensibly cautiones it customers “Their relative abundance may not ensure the value will hold over time”.

Whatever happens to future LGD retail prices, the category has got itself into the American consumer psyche and that won’t easily change, although there are also two sides to this story. I heard of a jeweller who was recently asked by a HNWI to make a replica of her 8-carat natural diamond ring so she could wear it travelling. The original ring cost $500,000 but he sourced an equivalent LGD for $5,000, and apparently she was absolutely thrilled with it. The question is, will she buy natural again? On the other hand, if in the future a consumer could buy (for example) a 2-carat LGD engagement ring for below $200, how pleased would their fiancé be to receive it – Walmart recently had a 2-carat LGD ring for sale for only $257. How romantic!

The US bridal market (size over quality) is dominated by larger, lower quality diamonds. Since similar sized LGDs are cheaper (or you get a much better quality LGD), either that market disappears, or demand only reappears aner prices have fallen sharply (already happened). It is also likely that LGDs will replace small, lower quality natural diamonds in fashion jewellery – as they may replace the smaller stones in high-end pieces of natural diamond jewellery. Diamond mining companies whose profitability rely on these categories of diamonds probably need to find a new value proposition, or their days may be numbered.

For those in the natural diamond industry who can adapt, there is huge potential. For those that don’t, as the saying goes, “Kodak never saw it coming either”.

Except Kodak did see it coming; they just didn’t know what to do about it. Kodak was killed off by digital photography which ironically, they invented, patented, but didn’t know how to exploit it, so they franchised the technology and made a fortune until their patents expired, and then went bust. Have LGDs done the same to natural diamonds? “No”, the opposite; their success is forcing a complacent industry to change. Have they changed the paradigm? “Completely”.

Gem Diamonds has now recovered twice as many +100 cts diamond this year than during the whole of 2023.

The UK-based company today announced a 129.71 carat Type II white diamond from its Letseng mine, in Lesotho.

It’s the 10th +100 cts diamond of 2024. Historically the mine averages eight per year, but last year it recovered only five.

The spike in high-value recoveries has helped push up revenue at Gem. Earlier this month it reported a 9 per cent increase in its first half earnings to $77.9m.

Letseng 70 per cent owned by Gem and 30 per cent by the Lesotho government is the highest dollar per carat kimberlite diamond mine in the world.

Pic courtesy Gem Diamonds, shows the 129.71 ct stone.

The US has added the prominent jewelry brand Miuz and the diamond cutter Kristall to its list of sanctioned companies in Russia.

Kristall, Russia’s largest diamond cutter, is now on the Specially Designated Nationals (SDN) List administered by the US Treasury Department.

Alrosa, its parent company has been on the list since April 2022, shortly after Russia invaded Ukraine. Kristall, based in Smolensk, has been part of the Alrosa group since 2019.

Miuz Diamonds, which has production facilities in Moscow and Perm and a chain of 300 retail outlets, has also been added to the list.

Miuz is part of the Ruiz Group of diamond and jewelry enterprises, linked to Israeli billionaire Lev Leviev.

It is not clear why the companies were not sanctioned sooner.

Kristall and Miuz are among almost 400 individuals and entities in Russia and beyond its borders that were added to the SDN list last Friday (23 August).

“Russia has turned its economy into a tool in service of the Kremlin’s military industrial complex,” said Deputy Secretary of the Treasury Wally Adeyemo, announcing the additions.

“Treasury’s actions today continue to implement the commitments made by President Biden and his G7 counterparts to disrupt Russia’s military-industrial base supply chains and payment channels.”

The Office of Foreign Assets Control (OFAC) has issued new licenses under the Russian Harmful Foreign Activities Sanctions Regulations, allowing for the sale of diamond jewellery and loose gem-quality diamonds imported before recent sanctions were implemented. This significant policy shift permits goods that were previously prohibited to re-enter the market.

Under the new guidelines, diamond jewellery purchased before March 1, 2024, as well as loose diamonds of 1 carat or larger bought before that date, and those of at least 0.50 carats purchased before September 1, 2024, can now be sold. The relaxation for loose diamonds will remain in effect until September 1, 2025.

However, starting September 1, 2024, the next phase of G7 diamond sanctions will impose restrictions on all goods of 0.50 carats or above from Russia, regardless of where they are cut and polished. This phase of sanctions is set to take effect next Sunday, despite substantial opposition from various industry stakeholders.

In response, the Jewelers Vigilance Committee has reported that the United States is considering supporting a delay in the implementation of these sanctions. This potential delay, which aligns with the European Union’s proposed extension to March 1, 2025, aims to provide additional time to resolve the intricacies of the sanctions and their impact on the diamond trade.